THEORETICAL ASPECTS OF FISCAL POLICY: TAXATION

Features of Resident

Nonresidents’ income from sources in the Republic of Kazakhstan

Procedure and deadlines for the payment of income tax at the source of payment

PROCEDURE FOR TAXATION OF THE INCOME OF NONRESIDENT INDIVIDUALS

Statement of anticipated individual income tax and individual income tax return

Direct deduction of expenses method

Procedure for the application of an international agreement with regard to the taxation of dividends, interest, and royalties

Навигация

THEORETICAL ASPECTS OF FISCAL POLICY: TAXATION

Налогообложение Резидентов и Неризидентов в Казахстане

86152

знака

3

таблицы

5

изображений

1. THEORETICAL ASPECTS OF FISCAL POLICY: TAXATION

1.1 Fiscal policy

Fiscal (lat. fiscalis - state) policy (politics) - is the aggregate of financial measures of the state on regulation of the governmental incomes and expenditures. It changes significant depending on put strategic tasks, as for example, anticrisis regulation, maintenance high employment, struggle with inflation.

The modern fiscal policy defines basic directions of use of financial resources of the state, means of financing and main sources of updating of treasury. Depending on concrete - historical conditions in different countries such policy (politics) has its own features. At the same time in Developed Countries is used set of common measures. It includes straight and indirect financial methods of regulation of economy.

To straight ways concern the means of budget regulation. By the means of the state budget are financed:

1) expense on expanding of reproduction;

2) unproductive expenditures of the state;

3) development of an infrastructure, scientific researches and etc.:

4) realization of structural policy (politics);

5) the support of military producers complex etc.

With help of indirect methods state influences on financial opportunity of the manufacturers of the goods and services and on the demand sizes of customer. The important role here plays the System Taxation. Changing the rates of the taxes on various kinds of the incomes, giving tax privileges, reducing free minimum of the incomes etc., state aspires to achieve probably steadier rates of economic Growth and to avoid sharp rises and falls of manufacture.

To number of the important indirect methods assisting accumulation of the capital, is the policy (politics) of the accelerated amortization. On the essence, the state exempts the businessmen from payment taxes with part of the profit, is artificial redistribute it in amortization fund. So, in Germany in the beginning 70 years on a number of industries on amortization it was authorized to write off till 20-30 of % of cost of a fixed capital in one year. In Great Britain in first year of introduction in using of the new equipment it was possible to deduct in fund of amortization 50 % of cost new instruments of manufacture.

However in these cases the amortization is written off in the sizes, that significant exceeding the valid deterioration basic capital, in consequences the raise of price on made with the help of this equipment production. If accelerated amortization expands financial opportunities of the businessmen, simultaneously it deteriorates the condition of realization of production and reduces purchasing power of population.

Depending on character of use direct and indirect financial methods distinguish two kinds of fiscal policy of the state:

a) Discretion

b) Non-discretion.

a) Discretion (lat. discrecio - working on itself discretion) the policy (politics) means the following. The state consciously regulates its expenditure and taxation with the purposes of improvements economic of situation of the country. At the same time government takes into account the following checked up on practice functional dependences between financial variable.

The first dependence: the growth of the state expenditures increases cumulative demand (consumption and investments). Thereof increase output and employment of the population. Is important to take into account, that state expenditures influence on cumulative demand the same as to investments (work as the animator of investment which has developed J. Keynes). The animator state expenditures MG shows, how much grows total national product D GNP in result of increase of these expenditures DG:

D GNP =DG ' MG

It is natural, that at reduction of state expenses G reduces the volume of GNP.

Other functional dependence shows, that increase the sums of the taxes are reduced the personal available income of household. In this case are reduced demand and volume of production and employment of a labor. And on the contrary: decrease (reduction) of the taxes conducts to increase of the consumer expenditures, production and employment.

The change of the taxation gives multiply effect. However the multiplier of the taxes is less than the multiplier of the investments and state expenditures. Actually increase in unit of a gain of the investments (and state expenditures) is directly influenced on increase in the volume of the GNP. At reduction of taxes, grows available income, however part it goes on the consumption, and stayed share is spent for the savings.

Mentioned functional dependences are used in discretion policy (politics) of the state for influence on business cycle. Certainly, this policy (politics) differs on different phases of a cycle.

For example, at crisis the policy (politics) of economic growth will be carried out.

In interests of growth GNP the state expenditures are increased, the taxes are reduced, and the growth of the expenditures is combined with reduction the taxes so that multiply effect on state expenses was more than multiply effect of the taxes. A result is reduction of recession of manufacture.

When there is an inflationary growth of manufacture (rise, induced by surplus of demand), the government will carry out policy (politics) that hold back business activity - reduces the state expenditures, increases the taxes. These measures are combined so that multiply effect of reduction of the expenditures was more, than multiplier of growth of the taxes. In result the cumulative demand is reduced and volume GNP accordingly decreases.

b) The second kind of fiscal policy - non-discretion, or policy of the automatic (built - in) stabilizers. The automatic stabilizer - economic mechanism, which without assistance of the state eliminates an adverse situation on different phases business cycle. Basic built - in stabilizers are tax receipt and social payments that are carried out by the state.

On a phase of rise, naturally, the incomes of firms and population grow. But at the progressive taxation the sums of the taxes increased even faster. In this period the unemployment is reduced, well being of needy families is improved. Hence, decrease the payments of the unemployment benefits and others social expenditures of the state. In a result the cumulative demand is reduced, and it constrains economic growth.]

The tendency of transfer payment spending to rise during recessions and fall during expansions results from the bases on which people qualify to receive these payments. People qualify to receive welfare programs only if their income falls below a certain level. They qualify for unemployment compensation by losing their jobs. When the economy expands, incomes and employment rise, and fewer people qualify for welfare or unemployment benefits. Spending for those programs therefore tends to fall. When economic activity falls, incomes fall. people lose jobs, and more people qualify for aid, so spending for these programs rises.

Taxes affect the relationship between real GDP and personal disposable income they therefore affect consumption expenditures. They also influence investment decisions. Taxes imposed on firms affect the profitability of investment decisions and therefore affect the levels of investment firms will choose. Payroll taxes imposed on firms affect the costs of hiring workers; they therefore have -impact on employment and on the real wages earned by workers.

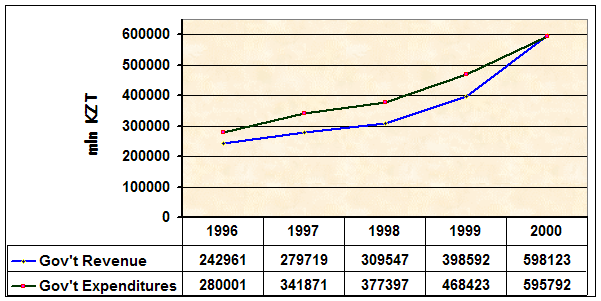

Exhibit below compares government revenues to government expenditures since I996. We see that government spending in Kazakhstan has systematically exceeded revenues, revealing an underlying fiscal deficit between 4 percent and almost 9 percent of GDP, entailing substantial public sector borrowing requirements. Until 1994, fiscal deficit had essentially financed through monetary expansion by the Central bank, with a highly detrimental effect on the rate of inflation during the period. Since then, the National Bank of Kazakhstan has adopted a more independent monetary policy, and fiscal deficits have basically financed either by the proceeds from privatization of state assets or by borrowing foreign loans.

Sources: Statistics Agency of RK, 2001

On a phase of crisis tax receipts automatically fall and reduced the sum of withdrawals from the incomes of firms and households. Simultaneously grow payments of social character, including unemployment benefit.

At result the purchasing power of the population is increased, that helps to overcoming recession of economy.

From mentioned above it is visible, how large place occupies taxation in financial regulation of macroeconomic. So we can conclude that the main direction of fiscal policy of the state is improving the legislations and practice collection of tax.

Let's take example for the most important version of the taxes – the income tax, which is established on the incomes of physical persons and on profit of firms. How the size of this tax is defined (determined)?

First is counted the total income - sum of all incomes that are getting by the physical and legal entities from different sources. From the total income by the legislation it is usual it is authorized deduct: 1) industrial, transport, the travelers and advertising expenditures; 2) various tax privileges (free minimum of the incomes; for example, in USA in 1990 this minimum was 2050 dollars; the sums of the donations, privilege for the pensioners, disable people etc.). Thus, taxed income is a difference between the total income and the specified deductions.

It is important to establish optimum tax rate (size of the tax on unit of taxation). The following rates of the tax differ:

· hard, which are established on unit of object independently on its cost (for example, motor vehicle);

· proportional, i.e. uniform percent(interest) of payment of the taxes independently on the sizes of the incomes;

· progressive, growing with increase of the incomes.

The practice shows, that at the extremely high rates of taxes discourages to work and to the innovation. Sharp increase in 60-70-е years in western countries of tax burden has resulted the negative consequences. It has caused " Tax revolts ", wide evasion from the taxes, promoted outflow of the capitals and flight of the addressees of the high personal incomes in the countries with one lower level of the taxation.

As it is known, in 70’s neo-conservators have put forward the theory of Supply. Its authors have established, that growth of the taxation renders adverse influence on dynamics of manufacture and incomes. Increase of the taxes at the expense of increase of their rates on certain stage does not compensate reduction of receipts in the state budget because of fast narrowing taxed incomes, and then it can be accompanied also by reduction of total sums of the budget incomes. In a result the high taxes render constraining influence on the offer of the capital, work and savings.

Basic task of economic policy representatives of the theory of Supply consider determining the optimum rates of taxation and both tax privileges and payments. Decrease (reduction) of the taxes is considered as a means capable to ensure Long-term economic growth and struggle with inflation. It will strengthen aspiration to receive huge incomes, will render the stimulating influence will increase by growth of production.

1.2 TaxationAs required by the Constitution of Kazakhstan, within the tax system of Kazakhstan, any taxes, levies, and other obligatory payments may be established only by the laws enacted by the Parliament of the Republic of Kazakhstan. Parliament may not delegate its constitutional powers to establish the tax system, taxes or levies, and sanctions for tax violations to the government or any other authority. Under the Constitution, laws in general and tax laws in particular enter into effect after the President signs them.

Tax legislation of the Republic of Kazakhstan consists of the Tax Code and Normative Legal Acts, and is regulated by International Agreements. Tax legislation is based on the principles of the mandatory nature of payment of taxes and other mandatory payments to revenue, certainty and equity of taxation, unity of the tax system and publicity of tax legislation. The Tax Code of the Republic of Kazakhstan establishes Kazakhstan taxes, levies, and general tax principles. A tax takes largest share of budget revenues (Appendix A).

Companies formed in Kazakhstan under Kazakhstan law are taxed on world-wide income. Income earned by a foreign company or person through a permanent establishment in Kazakhstan is taxed in Kazakhstan. Branches of foreign entities are taxed on Kazakhstan source income (where services are performed, not where paid for). Income from a Kazakhstan source to a non-resident and not related to a permanent establishment, is taxed at the source of the payment, and further, on the total income without deductions, excluding labor that is taxed as personal income.

Double Tax Treaties In December 1996, a treaty on the Avoidance of Double Taxation between the United States and Kazakhstan came into force. A number of treaties on the avoidance of double taxation were ratified in 1998. This includes agreements with the following countries: the Czech Republic (November 1998), France (November 1998), Sweden (July 1998), Bulgaria (July 1998), Turkmenistan (July 1998), Georgia (July 1998), Republic of Korea (July 1998), Germany (November 1998), and Belgium (November 1998).

Kazakhstan has double tax treaties with more than 20 countries, which generally follow the OECD Model Income Tax Convention.

| Withholding Tax Rates for Treaty Countries | |||||||

| Dividends | |||||||

|

| Major Rate | Legislative Rate | Major Holding | Interest (%) | Royalties | ||

| Azerbaijan | 10 | 15 | - | 10 | 10 | ||

| Belarus | 15 | 15 | - | 10 | 15 | ||

| Bulgaria | 10 | 15 | - | 10 | 10 | ||

| Canada | 5 | 15 | 10 | 10 | 10 | ||

| Czech Republic | 10 | 15 | - | 10 | 10 | ||

| Germany | 5 | 15 | 25 | 10 | 10 | ||

| Hungary | 5 | 15 | 25 | 10 | 10 | ||

| India | 10 | 15 | - | 10 | 10 | ||

| Iran | 5 | 15 | 20 | 10 | 10 | ||

| Italy | 5 | 15 | 10 | 10 | 10 | ||

| Kyrgyzstan | 10 | 15 | 10 | 10 | |||

| Lithuania | 5 | 15 | 25 | 10 | 10 | ||

| Mongolia | 10 | 15 | - | 10 | 10 | ||

| Netherlands | 5 | 15 | 10 | 10 | 10 | ||

| Pakistan | 12.5 | 15 | 10 | 12.5 | 15 | ||

| Poland | 10 | 15 | 20 | 10 | 10 | ||

| Russia | 10 | 15 | - | 10 | 10 | ||

| South Korea | 10 | 15 | 10 | 10 | 10 | ||

| Sweden | 5 | 15 | 10 | 10 | 10 | ||

| Turkey | 10 | 15 | - | 10 | 10 | ||

| Ukraine | 5 | 15 | 25 | 10 | 10 | ||

| United Kingdom | 5 | 15 | 10 | 10 | 10 | ||

| United States | 5 | 15 | 10 | 10 | 10 | ||

| Uzbekistan | 10 | 15 | - | 10 | 10 | ||

| * Belgium | 5 | 15 | 10 | 10 | 10 | ||

| Georgia | 15 | 15 | - | 10 | 10 | ||

| Iran | 5 | 15 | 20 | 10 | 10 | ||

| Mongolia | - | - | - | - | - | ||

| Rumania | 10 | 10 | - | 10 | 10 | ||

| Turkmenistan | 10 | 15 | - | 10 | 10 | ||

| France | 5 | 15 | 10 | 10 | 10 | ||

| Czech Republic | 10 | 15 | - | 10 | 10 | ||

| South Korea | 5 | 15 | 10 | 10 | 10 | ||

| a. Source: Guide on Taxation and Investment in Kazakhstan in 2002, Deloitte & Touche Notes: *double taxation treaties with 9 countries listed below are ratified only by Kazakhstan. | |||||||

Tax payment is based on the calendar year, with annual declarations due by end March of the following year (and tax payment within ten days of declaration). Annual financial statements are due April 30 following the reporting year.

Kazakhstan Tax Code, enacted in April 1995, currently apple an international taxation model based on principles of equity, economic neutrality and simplicity. The Parliament approved amendments to the Tax Code by a law dated July 16, 1999; the law was published and became effective August 3, 1999. Following amendments were made in 01 July 2001 and the New Tax Code has become effective January 1, 2002. The Ministry of State Revenues issued tax instructions clarifying the determination and payment of taxes. Resident persons and local enterprises pay taxes on worldwide income; foreign enterprises and non-residents pay taxes only on income from local sources. One is a resident and tax-liable for both direct and indirect income in Kazakhstan if he/she has been physically present in Kazakhstan for 183 days in any consecutive 12-month period.

The penalty for violation of foreign currency regulations constitutes 20 percent of the transaction amount. There are no limitations on the penalty amount to be charged.

All tax laws must be contained in the Tax Code, which covers taxation at all levels of government: central, oblast and local.

1.2.1. MAJOR TAXES and DUTIESEnterprise Profits Tax is levied on legal entities at the rate of 30%, but 20% in SEZs, and 10% on direct use of land as a sole production asset. All Kazakhstan and foreign legal entities doing business through a permanent establishment must register with the tax authorities regardless of whether they will pay taxes in Kazakhstan or not. Enterprise-related provisions in the Tax Code include: withholding on dividends and interest (15%); taxes on royalties, rentals and service fees; excise and local taxes, and land (10%), property and vehicle taxes; business registration fees, and fees to engage in selected activities. Branches of foreign enterprises operating in Kazakhstan pay a "branch profits tax" applied to their after-tax income. Most business expenses are deductible, including wages, but there are limits on deductibility of reserves for bad debts (actual losses deductible), and research and development. Depreciation is based on pooled asset accounts. Losses can be carried forward for three years.

Individual Income Tax: Individuals resident in Kazakhstan are subject to personal income taxation on their worldwide income. Nonresident individuals are subject to taxation only on income from Kazakhstan sources. Marginal rates after a small basic deduction, range from 5% to 30% with top rates applied to incomes over $33,700 per year. Most tax is withheld at the source of payment. The tax applies to non-residents' income that is sourced in Kazakhstan only, and to residents' income worldwide, including interest, dividends, capital gains and other income. Taxable income from a Kazakhstan source includes income received under a contract for work or from provision of services, when performed in Kazakhstan, regardless of where it is actually paid. Foreigners must register with local tax authorities and receive a Tax Registration Number within ten days of beginning work under contract in Kazakhstan, or when they become otherwise tax liable as a resident, or receive Kazakhstan sourced income at 500 times a monthly computed basis (about $4,500/year). Foreigners paid abroad must make quarterly estimated payments of income tax and a yearly income tax declaration (due March 31st following the tax year). Foreigners paid locally will have their individual income tax withheld at the source of payment and sent to the Budget by the employers.

Value Added Tax (VAT) applicable to all goods, work and services, including imports to Kazakhstan. The VAT on imports is usually 16%, and applies to services and goods. Credit for VAT paid on inputs, including Capital investment, is offset against tax on sales. No VAT is paid on exports except to other CIS countries, where by agreement, exports are fully taxed and imports are not taxed (origin principle).

The article provides that sales of textile, sewing, leather processing, and shoe industry products will be zero-rated (0 percent VAT on sales) for residents of Kazakhstan for sales within Kazakhstan. This change represents an important stimulus for the domestic light industry development.

Natural Resources Taxes include: bonuses paid for the right to resource exploration, royalties paid for the privilege of exploitation and excess profits taxes paid when profits exceed amounts anticipated in setting royalties. Tax rates are set by the Cabinet of Ministers and differ among resources, and are unique to each location and taxpayer. Prohibited: special benefits including lock-in of profits tax rates at conclusion of a Production Sharing Agreement (contract).

Securities Transaction Tax on new issues of non-government securities, including stocks and bonds: 0.5% of nominal value. Proceeds from secondary transactions are taxed at 0.3%, and 0.1% for government securities. Issuer is liable for tax on initial issues; buyer is liable for tax on secondary transactions.

Unified Land Tax is levied on peasants and farmers who use private or leased land in their business. The payers of the unified land tax are exempt from corporate income tax, VAT on sales, land tax, transport tax, and property tax. The rate of the unified land tax is set at 0.1 percent of the appraised land value (determined by the Land Committee).

Other Taxes: A fee for the use of the words "National," "Kazakhstan," "Republic," and their derivatives has been included into the list of taxes in the Tax Code, Business assets are taxed at 0.5% yearly, and individual-owned real estate is taxed at 0.1%. Vehicles are taxed annually depending on vehicle type and engine size.

Double Taxation. A foreigner won't be taxed in Kazakhstan if:

he/she is present in the country for less than 183 days in a year and his/her income is paid by a non-resident of Kazakhstan and his/her income is not taken as a deduction in computing corporate income tax by a permanent establishment in Kazakhstan.In not distinct cases, where the person is liable to taxation by law in his/her own country and in Kazakhstan, he/she is deemed to reside where he/he has a permanent home, or if he/she has a permanent home in both places, where his/her personal and economic relationships are centered, or in case this cannot be determined, where he/she currently lives and works ("habitual abode"). An individual may offset income tax paid in Kazakhstan against tax owing in his/her home country.

Additional Payments applicable to businessesPension Contributions: Employers must pay two categories of pension payment:

15% of payroll paid by companies monthly to the State Center for Pension Payments to be spent on existing pensioners and on state pensions for current employees; ?

10% of employees' gross salaries, not affecting the net pay, transferred for each employee to an accumulation pension fund of that employee's choice.

Excise :Excise duty is imposed on taxable items produced in, or imported into, Kazakhstan as well as on certain types of activities. Excise duty is imposed on alcohol and tobacco products, motor fuels, diesel, motor vehicles, salmon and sturgeon roe, firearms, crude oil and jewelry. Excise duty is also imposed on gambling businesses and lotteries. Taxable Products (1) AlcoholExcise duty is imposed on alcohol articles covered by Harmonized System numbers 2204 (wine from fresh grapes), 2205 (vermouth and other wines from fresh grapes flavored with plants or aromatic substances), 2206 (other fermented beverages), 2207 and 2208 (ethyl alcohol, spirits, liqueurs and other alcoholic beverages). Excise duty for alcohol products is levied at various rates in KZT per liter.

(2) TobaccoExcise duty is imposed on tobacco articles covered by Harmonized System numbers 2402 (cigars, cheroots and cigarettes), 2403 (other manufactured tobacco and tobacco substitutes, tobacco extracts and essences). Excise duty for tobacco products is levied at various rates in Euros per 1000 items.

(3) Motor FuelsExcise duty is imposed on certain motor fuels covered by Harmonized System number 2710 (diesel, gasoline and jet engine fuels). Excise duty for motor fuels is levied at various rates in EURO per 1000 kg.

(4) Motor VehiclesExcise duty is imposed on motor vehicles covered by Harmonized System numbers 8703 (motor cars and other vehicles designed for the transportation of persons). Excise duty for motor vehicles is levied at various rates normally in EURO per vehicle’s engine bulk or customs value.

Such taxes as corporate income tax, value added tax, personal income tax, and excise taxes account for the largest portion of budget revenues (Appendix B).

2. Features of Residents and Nonresidents taxation

Похожие работы

... курсовой разнице. Статья 103. Вычет налогов. Статья 104. Расходы, не подлежащие вычету. 2 Действующий порядок учета на предприятии ТОО «Жалыкпас» 2.1 Документальное оформление доходов и расходов Особенности бухгалтерского учета рассмотрим на примере организации ТОО «Жалыкпас». Это частное предприятие. ТОО "Жалыкпас" зарегистрировано в 1993г., является малым ...

0 комментариев